Payment Bond in Construction: Protection, Process, and Practical Use

On paper, every construction project runs on the agreed-upon payments outlined by clear contracts. In reality, when you are not a newbie, you know that it doesn’t always work this way.

A subcontractor may complete weeks of work, but face delayed payments. The same is true with suppliers delivering construction materials and waiting for weeks for invoices to be settled.

It is a reality of construction projects that also impacts the financial management workflows. When working with a new contractor for the first time, there is much more uncertainty.

However, there are payment protection tools like bonds that are used to protect the subcontractors and vendors. In this blog, I will explain the payment bonds in construction and show how they can act as financial protection for the parties.

Table of Contents

- What Is a Payment Bond in Construction?

- Payment Bond vs Performance Bond

- Payment Bond vs. Performance Bond vs. Mechanic’s Lien

- Payment Bond Rules in Different Countries

- How to Obtain a Payment Bond

- Filing a Claim

- Guarantees for Subcontractors and Vendors

What Is a Payment Bond in Construction?

In simple terms, a payment bond is a financial guarantee ensuring that the subcontractors, laborers, and material suppliers will be paid.

Imagine stepping onto a new project with a contractor you haven’t worked with before. But then payments start getting delayed, or worse, stop altogether. For subcontractors and suppliers, this situation turns into a serious financial strain. If the contractor fails to make payments, the surety covers the owed amounts.

It’s also important to understand that a payment bond does not work as construction insurance. It doesn’t protect the contractor who obtains it, but obliges the contractor to reimburse the surety.

Recommended reading:

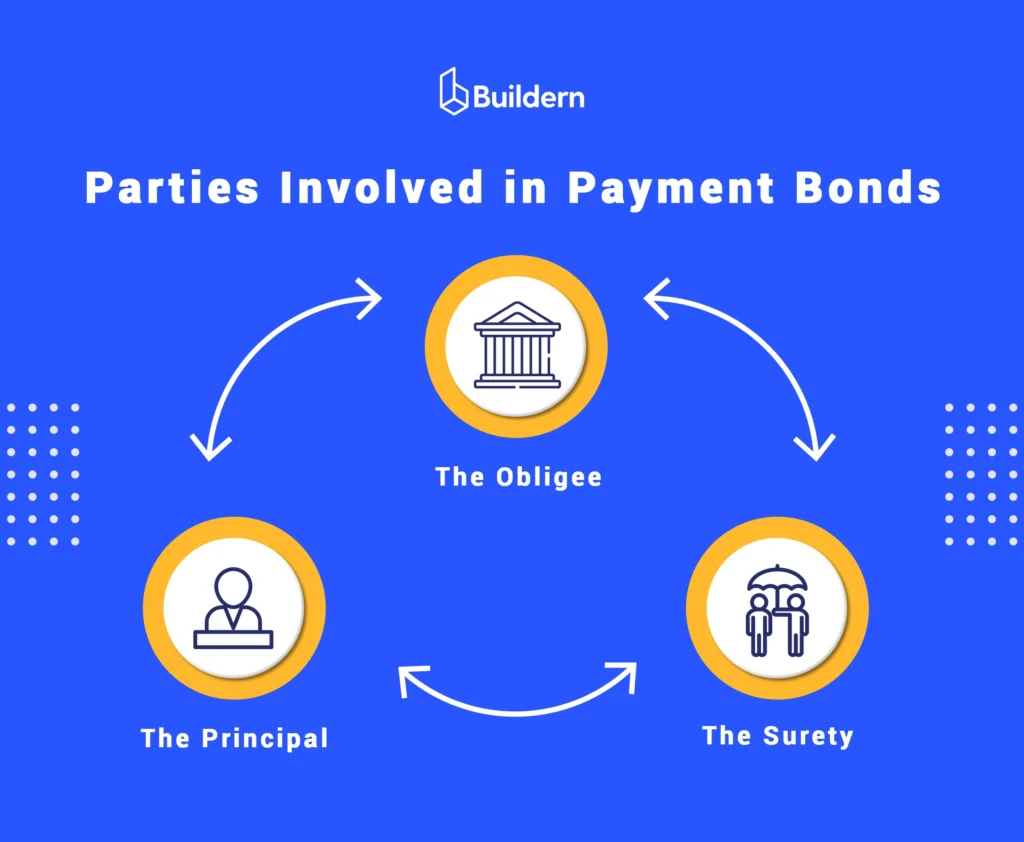

Key Players in Payment Bonds

A payment bond is a three-way agreement with each party having a specific role in ensuring payments are made and risk is managed properly.

- The Principal (general contractor) is a party that buys the bond. They are making a legal promise that they will pay their bills. If they don’t, and a claim is made, they are the ones who eventually have to pay the surety back.

- The Obligee (project owner): This is usually the person or entity who owns the building (or the government agency for public works). They require the bond because they want to ensure the project stays lien-free and that the workers are happy.

- The Surety: A company that issues the payment bond and provides the financial backing. If the Principal fails to pay, the Surety steps in to cut the check to the subcontractors.

To better understand how a payment bond in construction actually protects you, I’ll compare it with other common guarantee mechanisms.

Payment Bond vs Performance Bond

If you look at a construction contract, you will see that payment bonds and performance bonds are often mentioned together. While they both reduce risk, they serve very different purposes and protect opposite sides.

A payment bond protects the people doing the work, while a performance bond protects the project itself.

Thus, the payment bond is for the workers to protect subcontractors and vendors who provided the labor and materials and have to be paid what they were promised.

💡 Example 1: Payment Bond in Action

A general contractor hires several subcontractors for electrical, plumbing, and framing work, and the project progresses as planned. The general contractor runs into financial trouble midway through the project, leaving subcontractors unpaid. They filed a claim against the payment bond, and the surety ensured everyone got paid.

Thus, a performance bond is a guarantee for the owner that the contractor will complete the project according to the contract.

💡 Example 2: Performance Bond in Action

A contractor failed to complete a commercial project, leaving the owner with an unfinished building. The owner filed a claim against the performance bond, and the surety stepped in to finish the work or compensate for the losses

Recommended reading:

Payment Bond vs. Performance Bond vs. Mechanic’s Lien

A mechanic’s lien is a legal claim placed on the property where the work was performed. If a subcontractor or supplier isn’t paid, the lien gives them a legal right to seek repayment by potentially forcing the sale of the property to recover owed amounts.

Recommended reading:

This mechanism is more common on private projects and serves as a legal lever rather than a guaranteed payment. A payment bond in construction can be used by contractors working on public projects where filing a mechanic’s lien is not allowed.

Let’s compare these three protection mechanisms to understand which applies when:

| Feature | Payment Bond | Performance Bond | Mechanic’s Lien |

| Purpose | Guarantees that subcontractors, vendors, and laborers are paid | Guarantees that the project is completed as per the contract | Secures payment by placing a claim on the property if unpaid |

| Who Benefits | Subcontractors, suppliers, and laborers | Project owner | Subcontractors, vendors |

| Issuer | Surety company | Surety company | Legal claim filed by subs or vendors |

| Common Use | Public projects and contracts requiring bonded work | Large private and public projects | Mostly private projects |

| Key Differences | Focuses on payment fulfillment | Focuses on project fulfillment | Focuses on legal leverage via property |

Payment Bond Rules in Different Countries

Different regulations and industry practices mean that what works in one region might not apply in another.

Let me explain how payment bonds function in the United States, Australia, and the United Kingdom, including when they are required, how they are issued, and who oversees them.

Payment Bonds in the US

In the United States, payment bonds are often a legal requirement, especially when it comes to public construction projects. Their use is primarily governed by federal law and supported by state-level regulations.

For federal construction projects, payment bonds are required under the Miller Act. According to the Federal Acquisition Regulation (FAR), contractors must provide both performance and payment bonds for projects exceeding a certain amount.

- For contracts between $35,000 and $150,000, alternative payment protections may be used, including payment bonds, escrow accounts, or letters of credit.

- Below that threshold, bonds are generally not required.

Thus, payment bonds are mandatory for most mid-to-large construction contracts exceeding $150,000.

The purpose is simple: since subcontractors cannot file a mechanic’s lien on federal property, the payment bond becomes their primary legal protection for getting paid.

While the Miller Act applies to federal projects, each U.S. state has its own version known as the Little Miller Act. For example, in Florida, a payment bond is required for public construction projects over $200,000.

Payment Bonds in Australia

In Australia, there is no single federal equivalent of the US Miller Act. Instead, payment protection in construction is primarily governed by the Security of Payment (SOP) legislation, which operates at the state and territory level.

Each jurisdiction has its own SOP Act to protect subcontractors and suppliers from non-payment.

The closest equivalent to a payment bond in Australia is a contractual surety bond (also called a contract bond). However, unlike the US, their use on public projects is not universally mandated by legislation.

Payment Bonds in the UK

In the United Kingdom, there is no statutory equivalent of the US Miller Act, and payment bonds are not a legal requirement on public or private construction projects.

The UK has no mechanic’s lien system, and there is no specific concept of a contractor’s lien.

Under the Construction Act, a contractor’s primary remedy for non-payment is the right to suspend work. The Act does not grant a contractor any right over the property of the employer.

How to Obtain a Payment Bond

A payment bond is typically required before construction begins, as part of the contract between the project owner and the contractor.

You’ll usually see it in:

- Public projects (often mandatory)

- Large or high-risk private projects

- Situations where the owner wants to ensure strong financial management and reduce payment disputes

In construction workflows, once the payment bond is issued, it’s important to keep it easily accessible to all stakeholders. Using construction management software, contractors can store the bond and related documents in a centralized file section.

Getting a Payment Bond Step-by-Step

The responsibility to secure a payment bond falls on the contractor (principal). The process usually looks like this:

- Contractor finds a surety bond specialist.

- The surety reviews financial statements, credit history, past project performance, and cash flow stability.

- Underwriting and approval: If the contractor is deemed reliable, the surety approves the bond.

- The payment bond is issued and submitted to the project owner before work starts.

Cost of Payment Bond

💡 The cost of a payment bond, which is called premium, is typically a small percentage of the contract value. Rates can vary, but on average they stand between 0.5% to 3%. For example, if you have a $1 million contract and your premium rate is 1%, you pay $10,000.

The cost of a bond depends heavily on the financial profile of the general contractor. If you are a professional with a solid work history and working on projects within your area of expertise, you should generally expect a lower bond rate.

Additional cost factors are project duration, specialized high-risk trades, or maintenance/warranty periods.

Filing a Claim

If payments are delayed or not made at all, subcontractors and suppliers have a green light to file a claim. Here is a step-by-step process:

- Identify the Bond: Request a copy from the contractor or project owner to find the surety.

- Send Written Notice: Submit a formal claim to the surety and contractor, detailing the amount owed, project, and parties involved.

- Meet Deadlines: For federal projects (Miller Act), notice must be sent within 90 days of the last work (supply of materials, finish of the labor).

- Provide Documentation: Subcontractors or suppliers should include contracts, invoices, and change orders as proof.

- Resolution: If approved, the surety pays. Otherwise, the next step is to file a lawsuit.

💡 Tip: Always track deadlines carefully, as under the Miller Act, the one-year rule is strict.

Guarantees for Subcontractors and Vendors

While it’s typical to have a complex chain of contractors, subcontractors, and laborers, payment bonds are a cornerstone of financial security in the construction industry.

The risk of non-payment is high and can cause delays, disputes, and financial issues. So, payment bonds are a practical safety net that protects subcontractors, suppliers, and laborers.

In construction, trust is everything, and a subcontractor taking on a job is making a significant commitment by deploying workers, purchasing materials, and investing time. Thus, a payment bond assures that the commitment will be compensated regardless of what happens at the site.

When Is a Payment Bond Required on a Project?

Payment bonds are usually required on public projects and larger private projects. In the U.S., federal projects above $150,000 must have them, while state “Little Miller Acts” set varying thresholds for public works.

What is the Cost of a Payment Bond?

Payment bond typically ranges from 0.5% to 3% of the contract value, depending on the contractor’s financial stability, project size, and risk factors.

What is An Advance Payment Bond in Construction?

It’s a guarantee that any upfront payments to a contractor will be returned if the contractor fails to deliver the project as agreed, protecting the project owner from financial loss.